The days when you could trade cryptocurrency with total anonymity are over. If you run a crypto business or manage significant digital assets, the regulatory landscape has shifted from a loose collection of guidelines to a strict, global enforcement regime. By mid-2026, Know Your Customer (KYC) and Anti-Money Laundering (AML) compliance is no longer optional-it is the price of admission for operating in any major financial jurisdiction.

This isn't just about bureaucracy. It's about survival. Regulators worldwide have closed the loopholes that once allowed Virtual Asset Service Providers (VASPs) to operate in the shadows. From the United States' new stablecoin laws to Europe's unified MiCAR framework, the rules are tighter, the penalties are heavier, and the technology required to stay compliant is more sophisticated than ever before.

The Global Standard: FATF and the Travel Rule

To understand where we stand in 2026, you have to look at the foundation laid by the Financial Action Task Force (FATF). This intergovernmental body sets the global standards for combating money laundering. In 2019, they updated Recommendation 15, explicitly bringing virtual assets under their purview. But it wasn't until recently that these recommendations became hard law across borders.

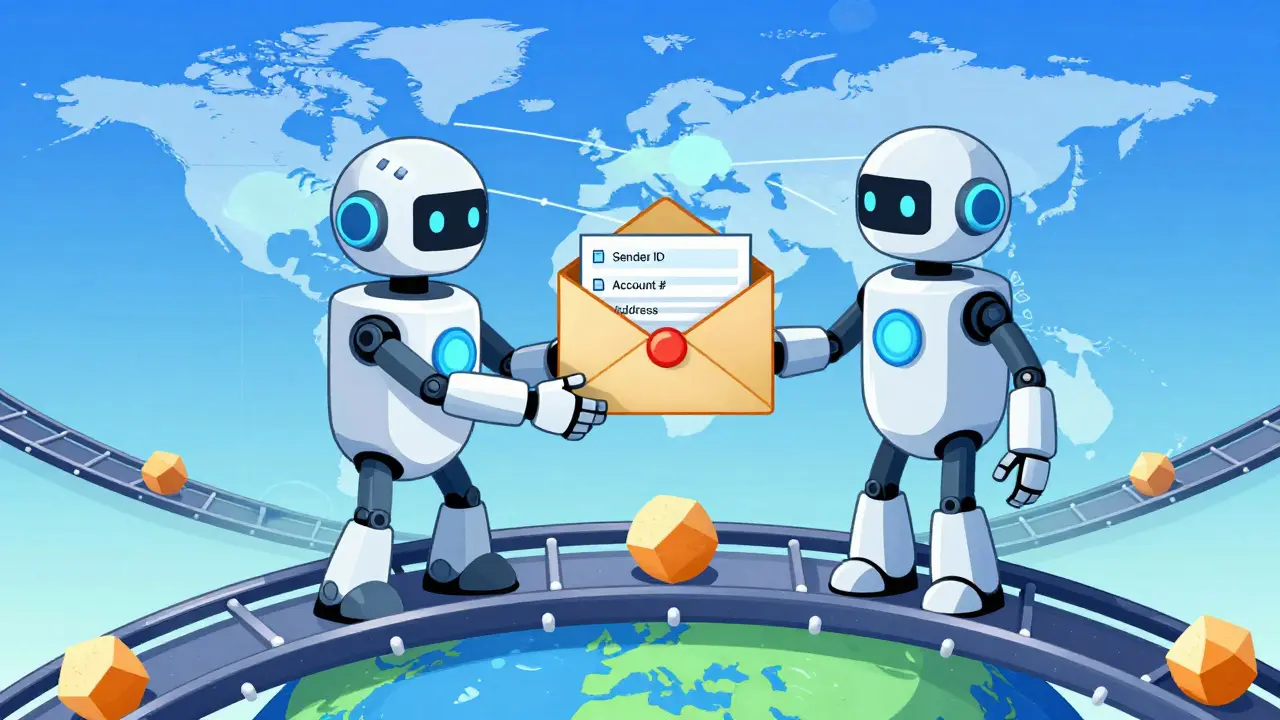

The cornerstone of this shift is the Travel Rule. Previously, banks had to share sender and receiver information for wire transfers above a certain threshold. The FATF extended this requirement to crypto transactions. Now, when you move funds between wallets or exchanges, the originating VASP must transmit specific data to the destination VASP. This includes:

- The name of the originator

- The originator's account number

- The originator's address, national identification number, or customer account number

In 2025 and early 2026, the scope of this rule expanded further. It now applies not just to centralized exchanges but also to certain decentralized finance (DeFi) gateways and non-custodial wallet services that facilitate fiat on-ramps. The goal is simple: make it impossible to launder money without leaving a digital trail that regulators can follow.

United States: The GENIUS Act and Stablecoin Scrutiny

The United States has moved from a fragmented approach to a more coordinated federal strategy. A major milestone was the advancement of the GENIUS Act in June 2025. Working alongside the STABLE Act, this legislation brings stablecoin issuers directly under the Bank Secrecy Act.

What does this mean for operators? It means that if you issue or handle stablecoins, you are subject to the same rigorous KYC and AML rules as traditional banks. There is no "non-negotiable" loophole here. You must implement robust identity verification, monitor transactions for suspicious activity, and report anything unusual to the Financial Crimes Enforcement Network (FinCEN).

The SEC and CFTC continue to scrutinize which tokens qualify as securities, but the Department of the Treasury has taken the lead on AML/CFT (Counter-Financing of Terrorism). For US-based businesses, this creates a clear, albeit demanding, path forward. Compliance is now a prerequisite for banking relationships. Without it, you cannot access the traditional financial system, which effectively kills your business model.

European Union: MiCAR and Unified Enforcement

Europe took a different route. Instead of piecemeal laws, the EU implemented the Markets in Crypto-Assets Regulation (MiCAR), which became fully applicable in December 2024. By 2026, all firms issuing Electronic Money Tokens (EMTs), Asset-Referenced Tokens (ARTs), and other crypto-assets within the EU must comply with this comprehensive framework.

MiCAR doesn't just set rules; it creates a single passport for crypto businesses. Once you are authorized in one member state, you can operate across the entire EU. However, the entry barrier is high. You need:

- Robust governance structures

- Transparent reserve management

- Strict consumer protection measures

- Integrated AML/KYC systems that meet EU-wide standards

Adding to this is the establishment of the Anti-Money Laundering Authority (AMLA). This central body seeks consistent enforcement across all member states, reducing the ability of bad actors to shop for lenient jurisdictions within Europe. If you are doing business in the EU, you are dealing with a unified, powerful regulator, not a patchwork of local agencies.

United Kingdom: Post-Brexit Rigor

The UK has carved out its own distinct regulatory path since Brexit. The Financial Conduct Authority (FCA) requires any firm exchanging, holding, or transferring crypto on behalf of customers to register under the UK's AML regime. Registration is not enough; you must actively demonstrate compliance.

The FCA expects:

- Detailed Customer Due Diligence (CDD) procedures

- Real-time transaction monitoring

- Maintenance of detailed records

- Submission of Suspicious Activity Reports (SARs) when necessary

In 2025, the UK strengthened its whistleblower protections through the Public Interest Disclosure (Amendment) Order. This encourages insiders to report misconduct, adding another layer of oversight. Additionally, the Register of Overseas Entities (OER) entered a new phase in July 2025, requiring disclosure of historical beneficial ownership changes. This makes it much harder to hide behind complex corporate structures.

The Bank of England continues to monitor stablecoin risks and explore a digital pound, while HMRC ensures tax compliance. The message from London is clear: crypto is a financial asset, and it will be treated like one.

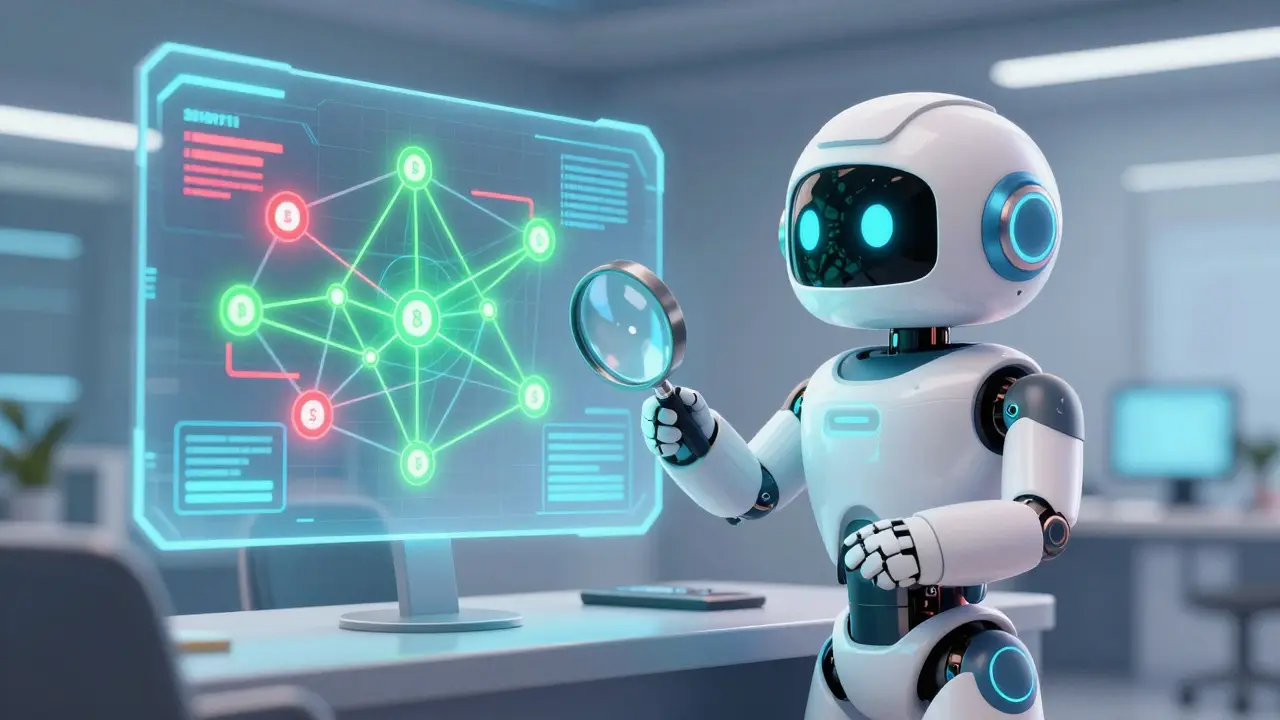

Technical Compliance: AI and Real-Time Monitoring

You cannot comply with modern AML rules using spreadsheets and manual checks. The volume of transactions and the speed of blockchain networks require technology-driven solutions. In 2026, leading crypto companies use AI-native transaction monitoring systems.

These systems perform several critical functions:

- Identity Verification: Automated KYC platforms verify government IDs, biometric data, and proof of address in seconds, reducing fraud and improving user experience.

- Transaction Monitoring (KYT): Know Your Transaction tools analyze blockchain data in real-time to detect patterns associated with money laundering, terrorist financing, or sanctions evasion.

- Sanctions Screening: With geopolitical landscapes shifting rapidly, compliance software must screen against dynamic sanctions lists. Falling short here leads to heavy fines and reputational damage.

- Predictive Analytics: Advanced systems use machine learning to identify emerging risks before they become problems, allowing for proactive mitigation.

Integrating these tools is challenging. You need to balance security with usability. If your KYC process is too cumbersome, users will leave. If it's too lax, you'll face regulatory action. The sweet spot involves layered verification-basic checks for low-risk activities and enhanced due diligence for high-value transactions.

Comparison of Regional Regulatory Frameworks

| Region | Primary Regulation | Key Enforcer | Focus Area |

|---|---|---|---|

| United States | GENIUS Act / Bank Secrecy Act | FinCEN / Treasury | Stablecoins, Banking Integration |

| European Union | MiCAR | AMLA / ESMA | Market Integrity, Consumer Protection |

| United Kingdom | FCA Registration / AML Regime | FCA / BoE | Transparency, Whistleblower Protections |

| Global Standard | FATF Recommendation 15 | National Authorities | Travel Rule, Cross-Border Data Sharing |

Challenges and Future Outlook

Implementing these requirements is expensive and complex. Smaller startups often struggle with the cost of compliance software and legal counsel. Larger enterprises face the challenge of integrating legacy systems with new blockchain analytics tools.

Another hurdle is cross-border consistency. While FATF provides guidelines, each country interprets them differently. A transaction that is legal in one jurisdiction might be flagged in another. Companies must build flexible compliance frameworks that can adapt to local nuances without breaking global standards.

Looking ahead to late 2026 and beyond, expect continued convergence. Regulators are sharing more data, and technology is making enforcement easier. The "Wild West" era of crypto is definitively over. Businesses that treat compliance as a core strategic function will thrive. Those that see it as a burden will likely fail.

For individuals, this means less privacy but greater security. Your assets are safer from theft and fraud, but your financial activities are more transparent. For businesses, it means higher barriers to entry but a more level playing field. The winners will be those who embrace transparency and invest in the right technology.

What is the FATF Travel Rule for crypto?

The FATF Travel Rule requires Virtual Asset Service Providers (VASPs) to share specific sender and receiver information during crypto transactions. This includes names, account numbers, and addresses, ensuring that crypto transfers have the same level of traceability as traditional bank wires.

How does MiCAR affect crypto businesses in Europe?

MiCAR provides a unified regulatory framework for crypto-assets in the EU. It requires firms to obtain authorization, adhere to strict consumer protection rules, and implement robust AML/KYC systems. Once authorized in one member state, businesses can operate across the entire EU.

What are the consequences of non-compliance with KYC/AML rules?

Non-compliance can result in severe penalties, including heavy fines, loss of license, and criminal charges for executives. It also damages reputation and makes it difficult to maintain banking relationships, which can effectively shut down a business.

Do DeFi platforms need to follow KYC rules?

Yes, increasingly so. While pure decentralized protocols are harder to regulate, any interface or gateway that connects users to DeFi using fiat currency or identifiable accounts is subject to KYC/AML requirements. Regulators are focusing on points of interaction where identity is known.

What technology do I need for crypto AML compliance?

You need automated KYC verification software, blockchain analytics tools for transaction monitoring (KYT), and sanctions screening databases. AI-driven platforms are recommended for real-time detection of suspicious patterns and managing the high volume of data involved.