As of 2026, there’s no single set of rules for cryptocurrency in the United States. Instead, each state has built its own system - and the differences are huge. If you’re running a crypto business, trading digital assets, or just holding Bitcoin, where you live matters more than you think. One state might treat you like a bank. Another might ignore you unless you hit a $500,000 transaction threshold. And in a few, you could get shut down for doing something that’s perfectly legal just across the border.

The truth is, crypto regulations by state are now the biggest factor in whether your business survives - or even gets off the ground. This isn’t about theory. It’s about real money, real legal risk, and real choices people are making every day. Some companies moved entire teams from New York to Wyoming just to avoid compliance costs. Others shut down operations in California because the registration process was too slow. And everyday users? They’re stuck in a system where their rights, protections, and access to services change depending on their zip code.

How We Got Here: No Federal Rules, Just Chaos

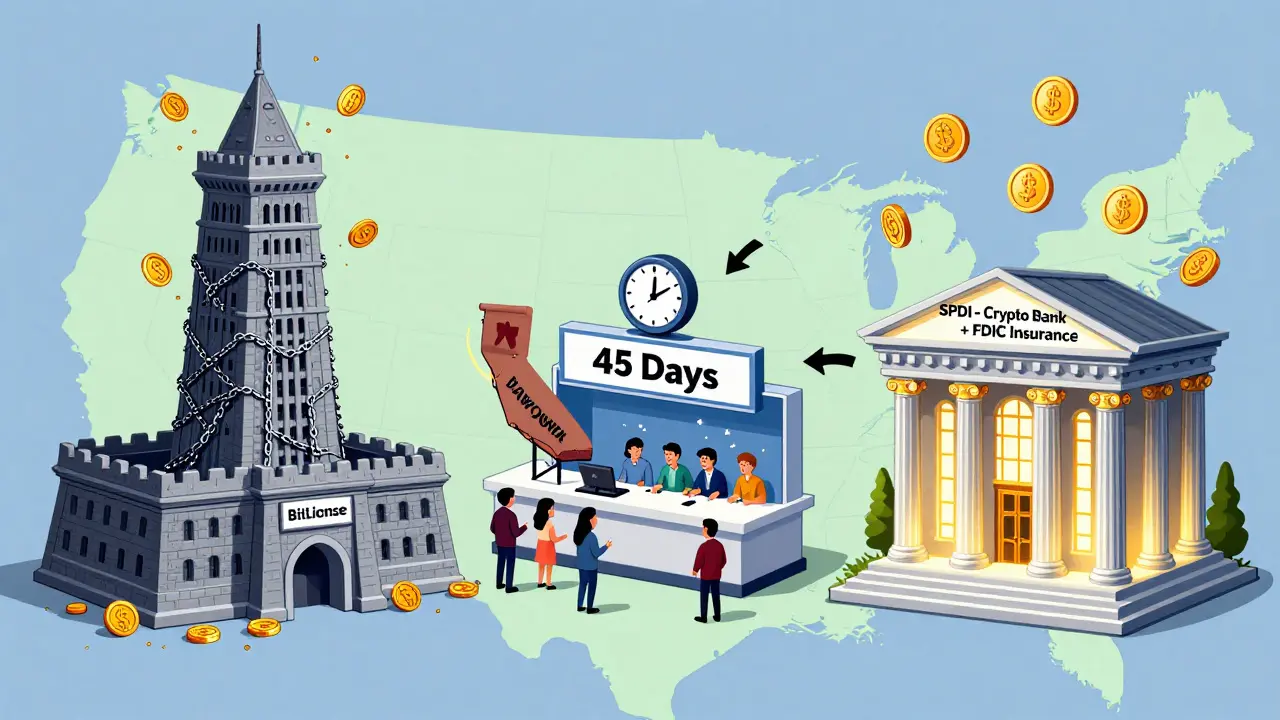

In 2015, New York dropped the first real bomb: the BitLicense. It was meant to bring order. Instead, it started a regulatory arms race. The idea was simple: if you’re handling crypto in New York, you need a license. But the cost? $5,000 just to apply. Minimum capital? $2 million. Ongoing audits? Monthly. By 2025, only 37 companies had a BitLicense - out of over 100 applications. Meanwhile, other states watched, then did the opposite.

Wyoming didn’t just create a rule - it built a whole new category: Special Purpose Depository Institutions (SPDIs). These aren’t regular banks. They’re crypto banks. Kraken Bank, Avanti Financial, and others now operate under state charters with FDIC insurance. That means they can take deposits, hold crypto, and offer loans - all under one roof. And guess what? They’re thriving. In 2024, these state-chartered crypto banks processed over $12.7 billion in transactions.

California took a middle path. No license needed unless you’re doing more than $500,000 a year in crypto transactions. Registration? 45 to 60 days. Fees? Under $1,000. No minimum capital. No onsite exams. By Q3 2025, 142 crypto firms were registered. That’s more than any other state. But it’s not perfect. The state has already launched 17 enforcement actions against unregistered businesses - and they’re not shy about it.

Meanwhile, states like Texas and Louisiana went even lighter. Texas doesn’t require a license at all. Just a basic cybersecurity plan. Louisiana exempts businesses under $35,000 in annual crypto activity. No paperwork. No fees. Just operate - as long as you’re small.

The Big Three: New York, California, Wyoming

These three states aren’t just examples - they’re archetypes. If you understand them, you understand the entire U.S. landscape.

New York: The Heavyweight

New York’s BitLicense is the strictest in the country. It covers 13 specific activities: buying, selling, storing, transmitting, exchanging, and even custody of crypto. If you do any of these, you need a license. And the requirements are brutal.

- Application fee: $5,000

- Minimum net capital: $2 million

- Annual compliance cost: $350,000 on average

- 80% of assets must be in NYDFS-approved cold storage

- Biometric access controls required

- Onsite examinations every 12-18 months

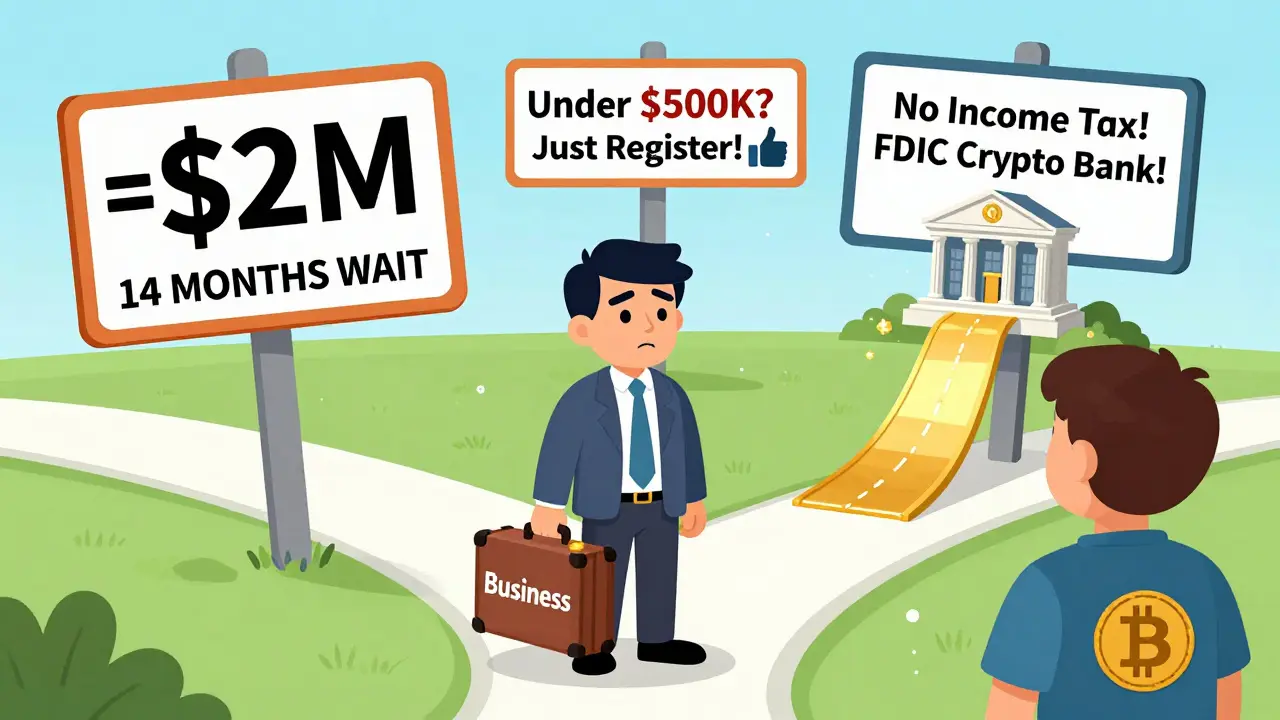

It’s not just expensive - it’s slow. The average approval time? 14.3 months. That’s over a year of waiting just to get started. And once you’re in? You’re locked in. Moving out is hard. Many firms that applied in 2020 still don’t have licenses. Some gave up. One crypto exchange founder told a reporter: "I spent $187,000 on compliance for zero revenue in NYC. Moved to Wyoming. Tripled volume in 18 months."

Users feel it too. Complaints take an average of 217 days to resolve in New York. In California? 38% faster.

California: The Middle Ground

California’s approach is pragmatic. You don’t need a license - just a registration - if you’re doing more than $500,000 in crypto volume per year. Below that? You’re free to operate. No state oversight.

Registration requires:

- Basic business info

- AML/KYC procedures

- Proof of insurance

- Annual renewal fee: $1,000

It’s not perfect. The Department of Financial Protection and Innovation (DFPI) has cracked down on unregistered firms. But compared to New York? It’s a breeze. And it’s working. California now has more registered crypto businesses than any other state. And the average resolution time for user complaints? Just 134 days - nearly half of New York’s.

Wyoming: The Crypto Haven

Wyoming didn’t just regulate crypto - it redefined it. In 2018, it created SPDIs. These are state-chartered banks that can hold crypto as deposits. They’re insured by the FDIC. They can lend. They can issue debit cards. They can even offer interest-bearing crypto accounts.

Requirements for an SPDI charter:

- $25 million minimum capital

- FDIC insurance

- State exam and approval (6-8 months)

- Compliance with federal AML rules

It’s not easy to get one - but once you do, you’re treated like a real bank. And companies are lining up. Kraken Bank, Avanti, and others now operate under this model. In 2024, Wyoming’s crypto sector generated $427 million in state revenue - 7.3% of its total income. That’s more than oil, mining, or tourism.

Wyoming also has no state income tax. No sales tax on crypto. No capital gains tax. For businesses and investors, it’s a magnet.

The Rest of the States: A Wild Patchwork

Forty-seven states have some form of crypto regulation. But most are a mess.

Some states require bonding - a financial guarantee that you’ll cover losses. Texas requires $25,000. New York requires $500,000. Others, like Arizona and Nevada, created "regulatory sandboxes" - safe zones where startups can test products without full licensing. Arizona’s sandbox led to a 34% faster growth rate in crypto startups than in non-sandbox states.

Then there are states like Massachusetts and Connecticut. They don’t have clear rules, but they’re aggressively going after crypto firms anyway. Massachusetts Secretary of the Commonwealth William Galvin said in October 2025: "The state-by-state approach creates a recipe for disaster." He pointed to $2.1 billion in crypto scams recovered in his state between 2020 and 2025.

Some states are trying to align with federal changes. The GENIUS Act, signed in September 2025, tried to set national standards for stablecoins. But 22 states are now suing to block it, claiming it violates state sovereignty. So now, even the federal attempt to fix this is fueling more chaos.

What This Means for You

Here’s the real question: What does this patchwork mean for you?

If you’re a business owner: Your location determines your costs, speed to market, and legal risk. Operating in multiple states? You’re likely spending $287,000 a year just on compliance - according to Goodwin Law’s 2025 analysis. That’s not R&D. That’s not marketing. That’s legal paperwork.

If you’re a trader or investor: Your rights depend on where you live. In Wyoming, you can hold crypto in an FDIC-insured bank account. In New York, you might be forced to use an exchange that’s overburdened with compliance and slow to respond to issues. In California, you get faster dispute resolution - but if your exchange isn’t registered? You have no recourse.

If you’re a developer or startup: You’re not choosing a city. You’re choosing a legal environment. The Blockchain Association’s 2025 survey found that 68% of crypto firms see state regulatory uncertainty as their top challenge. And 41% avoid certain states entirely.

There’s no "best" state for everyone. But there are clear patterns:

- Want to move fast? Go to California.

- Want to build a bank? Go to Wyoming.

- Want to avoid hassle? Avoid New York unless you have millions to spend.

What’s Next? Federal Rules Are Coming - But Not Soon Enough

The GENIUS Act was supposed to fix this. It requires stablecoins to be 100% backed by liquid assets. It creates a federal licensing system. It gives the CFTC authority over crypto trading. But it’s already under fire.

States like Texas and Wyoming are fighting it in court. They say it steals their power. Meanwhile, the SEC and CFTC are still arguing over who gets to regulate what. And everyday users? They’re caught in the middle.

By 2027, experts predict one of two outcomes: Either the federal government takes full control - wiping out state rules - or it officially recognizes a partnership where states keep their own rules, but they must meet federal minimums. Right now, it’s anyone’s guess.

One thing is certain: The current system is unsustainable. Companies are relocating. Talent is fleeing. Users are confused. And regulators are overwhelmed.

If you’re serious about crypto in the U.S., you need to know where you stand - not just legally, but practically. Because in 2026, your state isn’t just where you live. It’s your business strategy.

Which states have the strictest crypto regulations?

New York has the strictest rules through its BitLicense system. It requires a $5,000 application fee, $2 million in minimum capital, 80% cold storage of assets, biometric access controls, and annual compliance costs averaging $350,000. Only 37 licenses have been issued since 2015, despite over 100 applications. Massachusetts and Connecticut also have aggressive enforcement, even without clear laws.

What is the easiest state to start a crypto business?

California is the easiest for small to medium businesses. If you do less than $500,000 in annual crypto volume, you don’t need to register at all. For larger operations, registration takes 45-60 days, costs under $1,000, and requires no minimum capital. Wyoming is easier for banks and institutions, but requires $25 million in capital - not feasible for most startups.

Can I operate a crypto business in multiple states?

Yes, but it’s expensive. Multi-state operators spend an average of $287,000 annually just on regulatory compliance - not including legal teams or software. Each state has different definitions of "money transmission," different reporting rules, and different licensing requirements. Many firms avoid operating in New York and Massachusetts for this reason.

Does Wyoming really allow crypto banks?

Yes. Wyoming created Special Purpose Depository Institutions (SPDIs) in 2018. These are state-chartered banks that can hold crypto as deposits, offer interest, and issue debit cards - all with FDIC insurance. Kraken Bank and Avanti Financial Group operate under this model. Over $12.7 billion in crypto transactions flowed through SPDIs in 2024.

What happens if I ignore state crypto laws?

You risk fines, shutdowns, or criminal charges. California has launched 17 enforcement actions against unregistered crypto firms. New York has shut down exchanges for operating without a BitLicense. Massachusetts seized assets from crypto scams. Even if you think you’re small, if you’re handling over $500,000 in crypto annually in California - or any activity in New York - you’re already in violation.

Austin King

Love how Wyoming just said "screw it" and built something actually useful. No wonder Kraken and Avanti are thriving there. It’s not about being permissive-it’s about being smart.

Real innovation happens when you stop treating crypto like a threat and start treating it like infrastructure.